Mesothelioma and Life Insurance Options People Often Misunderstand

When someone hears “you can get money from life insurance,” they often think it only means one thing: a payout after death. With a diagnosis like mesothelioma, families sometimes need help much sooner than that. The confusing part is that there is more than one way a life insurance policy can create financial support, and each option has different rules, timing, and paperwork.

The biggest misunderstanding is thinking the diagnosis alone decides everything. It doesn’t. What matters just as much is the policy type, the size of the policy, how long it has been active, and whether premiums are still being paid. Some policies are easier to evaluate than others. Some can be sold. Some cannot. It depends on the contract, not just the health situation.

Not every policy works the same way.

A term policy and a permanent policy behave differently. Even within term policies, “convertible” and “non-convertible” can change what options are available. Policy ownership and beneficiary details also matter. Sometimes the insured person is not the owner. Sometimes there is a trust involved. These details sound small, but they can slow things down if they are discovered late.

If families check the basics early policy type, face value, premium amount, and ownership it usually saves time later. It also prevents unrealistic expectations, which is honestly a big problem when people are already stressed.

Timing is not always fast, so planning matters.

Another common misunderstanding is speed. People hear “cash option” and assume it means immediate money. In reality, the timeline depends on how quickly documents can be collected and reviewed. Medical records, policy illustrations, and carrier verification can take time. It’s not always anyone’s fault; it’s just how the process works.

When families understand that there is a process, they plan better. They can avoid last-minute panic, avoid signing something unthinkingly, and avoid pushing decisions when they are exhausted.

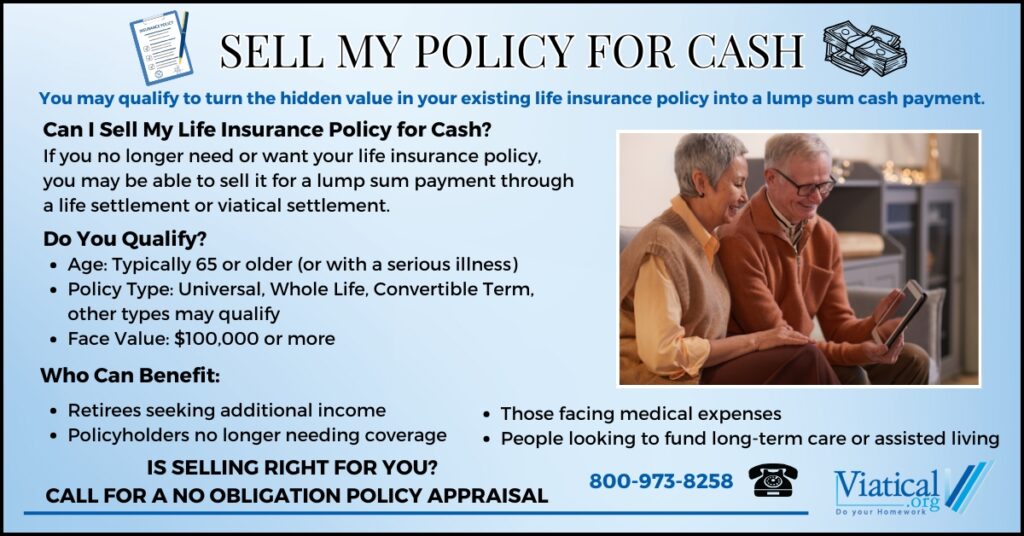

Life settlements and viatical settlements are not the same as a payout.

A life insurance payout is a death benefit paid to beneficiaries after a claim is approved. A life settlement or viatical settlement is different: it’s when a policyholder may be able to sell an existing life insurance policy to a third party for a cash amount, while still living. This is usually considered when the policy is no longer needed, premiums are too expensive, or money is required for care and daily expenses.

For serious illnesses, people often ask:

· “Can the policy help us now?”

· “Do we have to keep paying premiums?”

· “What if we don’t want the policy anymore?”

Those are settlement-type questions. The answer depends on eligibility and policy details, not just need.

What usually affects eligibility and value

A few factors are commonly reviewed during a settlement evaluation:

· Policy face value (death benefit amount)

· Policy type and how long it has been active

· Premium amount and whether it is current

· Age and health status (with supporting medical records)

· Carrier and policy terms

None of these factors works alone. A big policy with huge premiums may be harder to keep. A smaller policy might still be useful if premiums are manageable. It’s a combination.

Documentation is the part that people underestimate

The process is not “just one form.” A clean file matters. Missing pages, outdated documents, or unclear medical records can slow everything down. Families who keep things organised usually get clearer answers faster, even if the final result is “not eligible.” Clear information leads to clear decisions.

Family conversations matter more than people admit

These decisions usually involve spouses, adult children, caregivers, and sometimes even financial advisors. When one person has the documents and everyone else is guessing, confusion grows. A simple shared conversation about the policy, what it costs, and what the goal is can keep things calmer. It doesn’t solve everything, but it stops misunderstandings from turning into arguments.

With mesothelioma, the hardest part is that financial needs don’t always match insurance timelines. That’s why it helps to understand the difference between a traditional death benefit payout and options like a viatical or life settlement, which may provide cash while the insured person is still alive. On viatical.org/blog/, readers can learn how these options work, what paperwork is usually required, and what realistic timelines look like. The best move is to review the policy early, keep records ready, and ask direct questions so decisions are made with clarity, not pressure.

check out our site for more details.

Comments

Post a Comment